Little Know Secret of the 1% to keep their

Retirement Tax-Free!

Top #3 Reasons why your financial advisor has not

told you about this little know secret of the 1%

Reason 1: Most financial advisors don’t know that an insurance account like this exists. Nor, do they know how to set it up properly for the account holder.

Reason 2: Most financial advisors recommend financial vehicles that the company they've contracted with tells them to recommend or vehicles they receive the most compensation.

Reason 3: Straight-up lack of knowledge and as a result, less than 0.07% of Americans have what we call a "Tax-Free Retirement Protection/ Living Benefits Account" setup -while more than half the population has a taxable 401(k) or similar tax-deferred retirement account like a Roth IRAs.

The Problem with Your Tax-Deferred 401(K) or IRA Is...

You have to pay taxes on a larger portion of the money (when you take money out, the account value will be higher due to gains over the years—meaning you will be taxed heavily).

Your money is NOT liquid (you can’t access your money any time you want, and if you do, you're required to pay large penalties).

You are limited to how much you can invest or contribute (plans with most tax benefits have funding limits).

Your money is NOT guaranteed (The money in your 401(k) or IRA soars with the market, and plummets with the market.) One bad year like 2008 could cause you to lose 50% of your retirement and be forced to continue to work.

You are required to report your earnings to the IRS. (Everything in a 401(k) or IRA is, Uncle Sam’s business)... and we know they will get their "fair share."

You could pay higher taxes in the future. After 2025 many of the tax changes that lowered current tax rates will be gone. In 2026 those changes expire and taxes could go up significantly..

With A Tax-Free Retirement Account:

You earn 30-40 times more interest than with a regular bank account. (Historically, qualified individuals earned 3-6% a year.)

Your money is Liquid (All money put into and made in your cash value account is cash—you can withdraw any amount—at any time—without fear of penalty). It's YOUR money.

You are NOT required to report earnings to the IRS. (The IRS doesn’t classify income as “income” inside this kind of account . Not Uncle Sam’s Business. IRS Code 7702)

And there are many more wonderful fiscal things you can do with an account like this. With Tax-Free Retirement Protection your money, hard-earned retirement savings, and peace of mind are all protected

When structured correctly, the account can give a Tax-Free Income for Life

These accounts have a Tax-Free Death Benefit

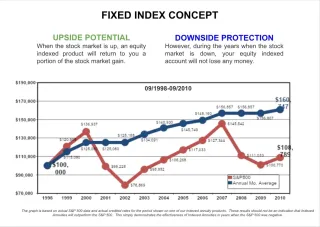

Your account is protected from market fluctuations

Think of it as a ROTH IRA with a Living and Death Benefit attached to it!

Infinite Bank Concept / Velocity Banking / Privatized banking all are concepts leveraging the power of Cash-Value Life Insurance.

In the News

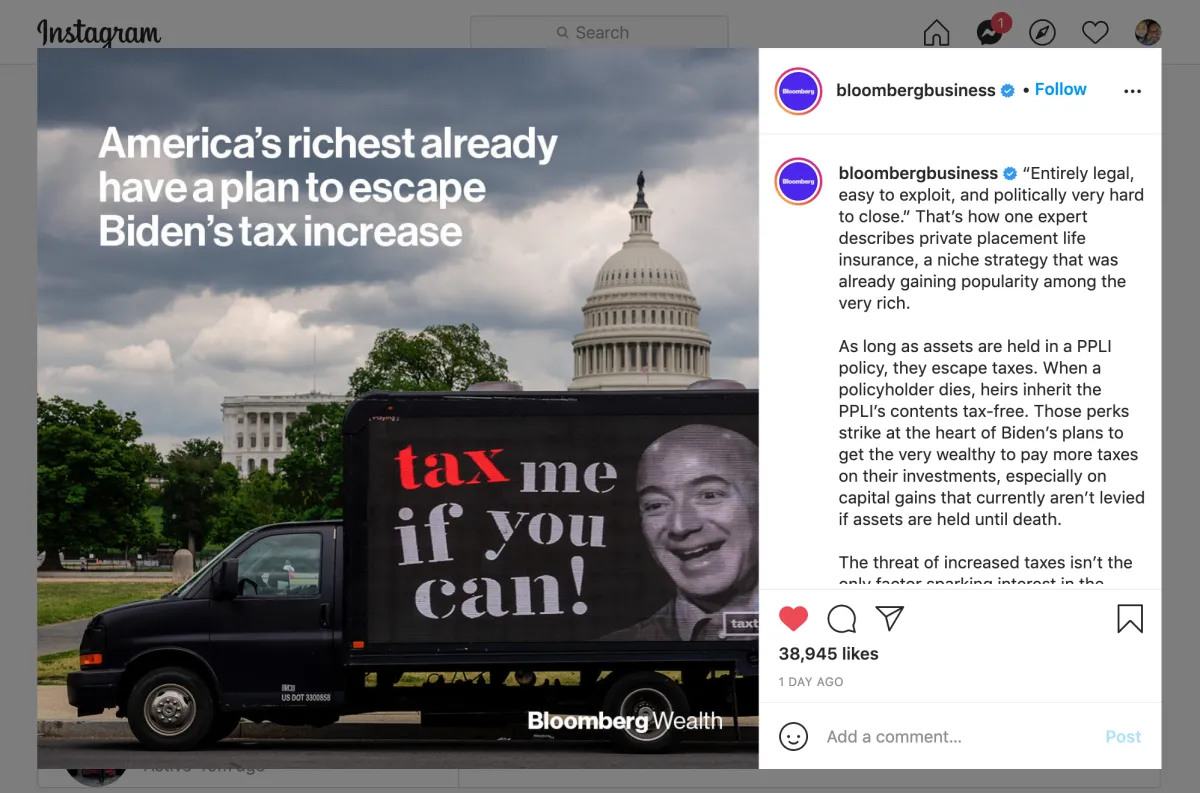

“Entirely legal, easy to exploit, and politically very hard to close.” That’s how one expert describes private placement life insurance, a niche strategy that was already gaining popularity among the very rich.

As long as assets are held in a PPLI (IUL) policy, they escape taxes. When a policyholder dies, heirs inherit the PPLI (IUL) , and Participating Whole Life, contents tax-free. Those perks strike at the heart of Biden’s plans to get the very wealthy to pay more taxes on their investments, especially on capital gains that currently aren’t levied if assets are held until death.

The threat of increased taxes isn’t the only factor sparking interest in the policies. A little-noticed change in U.S. insurance law at the end of 2020 also makes them a more powerful tool." - Bloomberg Business

Jim Harbaugh agrees to increased compensation

in form of life insurance- 2016

Michigan Head Football Coach Jim Harbaugh

Michigan and football coach Jim Harbaugh agreed to a contract amendment that will increase total payments from the school to $9 million in 2016.

In addition to paying a $5 million salary for each of the remaining six years on his deal, Michigan also will loan Harbaugh $4 million in 2016 and an additional $2 million for the following five years to pay the premium on a life insurance policy. The first $2 million loan was made June 3, according to records obtained Wednesday via a Freedom of Information Act request. Each additional $2 million payment will be made in December starting later this year.

As long as the insurance policy stays active, Harbaugh does not need to repay the loan until he dies. At that time, the university can recoup its original investment and the rest of the insurance payout would go to whomever Harbaugh chooses as his beneficiaries. Should the policy be stopped at any point, Michigan would still be entitled to get its money back from the insurer.

Source ESPN

Frequently Asked Questions: Tax Free Retirement Accounts:

What is a Tax Free Retirement account?

An IUL, is insurance policythat combines the protection of life insurance with the potential for cash accumulation through an investment account that is linked to a stock market index.

How an Tax Free Retirement account work?

The premiums you pay for an IUL are divided between the cost of insurance and an investment account. The investment account is credited or tied to a stock market index, such as the S&P 500, which is used to determine the amount of interest credited to the account.

What are the benefits of a Tax Free Retirement account?

The benefits of an TFRA , or an IUL include tax-deferred growth, downside protection, a death benefit for beneficiaries, and the potential to earn higher returns than traditional fixed-income investments.

How does the death benefit of a Tax Free Retirement account work?

The death benefit in an IUL is a guaranteed minimum amount that is paid out to beneficiaries upon the insured's death. The amount of the death benefit is based on the policy's face value and the performance of the investment account.

Can I withdraw money from my Tax Free Retirement Account?

Yes, you can withdraw money from your IUL, but there may be penalties for doing so before a certain time period has passed. You can also take out a loan against the cash value of the policy.

Are there any tax implications with?

An IUL is funded with after-tax dollars, but the growth on the investment account is tax-deferred. Additionally, withdrawals are tax-free as long as they are less than the total amount of premiums paid into the policy.

How much can I contribute to a TFRA?

There is no specific contribution limit for a TFRA or an IUL, but the amount you can contribute is limited by the policy's face value and the insurance company's guidelines. Click Below for a one-on-one consultation with a licensed professional.

How do I choose a TFRA?

When choosing an IUL, it is important to consider factors such as the insurance company's financial strength, the policy's fees and charges, the index used for the investment account, and the policy's death benefit and surrender charges.

Are there any risks associated with a TFRA?

As with any investment, there are risks associated with an IUL, including market volatility and the potential for the insurance company to default on its obligations. However, most TFRA (IUL) come with a "Floor," so while the market may go down you have a floor.

Is a TFRA right for me?

Whether a TFRA, IUL or Participating Whole Life aka Velocity Banking Concept, is right for you depends on your individual financial situation and goals. An IUL may be a good fit for those looking for tax-deferred growth, downside protection, and the potential for higher returns than traditional fixed-income investments. It is important to consult a licensed agent to determine if a TFRA is appropriate for you.

Do You Qualify for A Tax Free Retirement Account?

A Tax-Free Retirement Protection Account is NOT available just to the super-rich…However: an insurance account like this can only be technically set up if you, or your family, qualify for it.

Take a Quick 5-Second Survey to see if you qualify:

All right reserved | Privacy Policy | Copyright 2026|TaxFreeRetirement101